Mortgage is an important part of the process of buying a home or real estate. However, not everyone understands the types of mortgages available on the market. Each type of mortgage has its own characteristics and advantages and disadvantages, helping borrowers choose the option that best suits their financial situation and personal needs. This article will introduce in detail the most popular types of mortgages today, helping you better understand and make smart decisions when borrowing money.

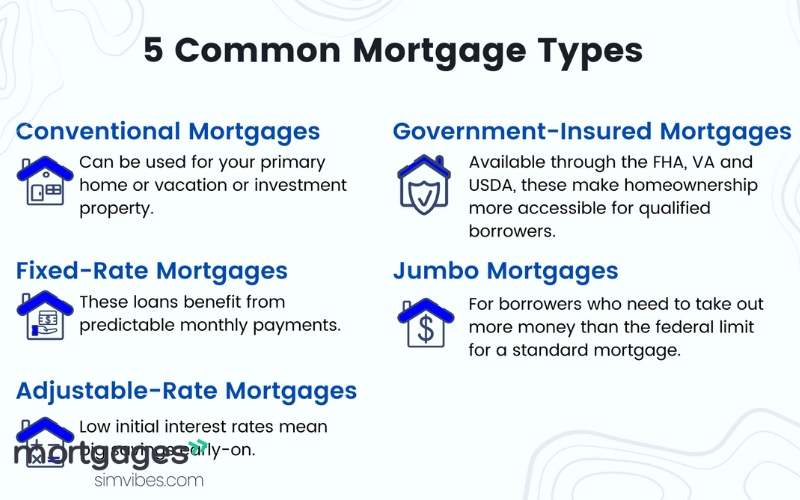

1. FIXED-RATE MORTGAGE

Fixed mortgages are the most popular type of loan on the market. The characteristic of this type of mortgage is that the interest rate will not change throughout the loan term, from the beginning to the end of the contract. This brings stability and predictability of monthly payments to the borrower.

The biggest advantage of fixed mortgages is financial stability. You don’t have to worry about interest rates rising over the life of the loan, making it easier to plan your finances and avoid unforeseen fluctuations. However, fixed mortgage rates are typically higher than adjustable-rate mortgages in the beginning, and the total loan repayments will be higher compared to other types of loans with variable interest rates.

2. ADJUSTABLE-RATE MORTGAGE (ARM)

An adjustable-rate mortgage (ARM) is characterized by an interest rate that changes over time, usually after a fixed period of time, such as 3, 5, or 7 years. The initial interest rate of an ARM is usually lower than that of a fixed mortgage, which helps to ease the initial financial burden on the borrower. However, over time, the interest rate may adjust and increase depending on underlying interest rate indices such as the Federal Reserve’s interest rate.

One of the advantages of ARMs is the ability to save money on interest in the early years when interest rates are low. However, the biggest disadvantage is financial instability, as interest rates can rise and increase monthly payments in the future. Therefore, this type of mortgage is suitable for people who have financial flexibility or anticipate that their income will increase in the future.

3. FIXED-RATE AND ADJUSTABLE MORTGAGE (HYBRID MORTGAGE)

A hybrid mortgage is a combination of a fixed-rate mortgages and an adjustable-rate mortgage. With this type of mortgages, the interest rate will be fixed for a certain period of time, usually from 3 to 10 years. After that, the interest rate will adjust and change according to the prime rate index.

The advantage of a hybrid mortgage is that you can take advantage of low interest rates in the early years, while still having the protection of a fixed interest rate. After the fixed period, when the interest rate can change, the borrower will face fluctuations. Therefore, this type of mortgage is suitable for those who can afford stable payments in the early stages, but are still prepared for expenses that may change later.

4. INTEREST-ONLY MORTGAGE

An interest-only mortgage allows the borrower to pay only the interest for an initial period, usually 5 to 10 years, without having to pay the principal. After this period, the borrower will begin to pay both the interest and the principal, causing the monthly payment to increase significantly.

One of the advantages of an interest-only mortgage is that it helps the borrower reduce the financial burden in the early years. However, the disadvantage is that after the interest payment period ends, the borrower will face a much larger payment, due to having to pay both the principal and interest. This type of mortgages is often used by real estate investors to reduce initial costs, but it can also cause great financial pressure when it comes to paying off the principal.

5. BALLOON MORTGAGE

A balloon mortgage is a type of mortgage that has a large payment at the end of the loan term, usually after 5, 7 or 10 years. During the loan term, the borrower will only pay a small portion of the principal and interest. However, at the end of the loan term, they will have to pay a very large amount again, called the “balloon”.

The advantage of a balloon mortgage is that you will be able to have a low monthly payment throughout the loan term, which helps to ease financial pressure. However, the biggest disadvantage is that you will be faced with a huge payment at the end of the loan term, which can cause financial stress if not prepared in advance. This type of mortgage is suitable for people who plan to refinance the loan or sell the property in a short period of time.

6. LOW-INTEREST MORTGAGE

A low-interest mortgage is a popular option for first-time homebuyers who don’t have the money to make a large down payment. Instead of requiring a large down payment, borrowers make a smaller down payment than they would with a traditional loan.

A big advantage of this mortgages is that it makes it easier for borrowers to buy a home without having to save up a large amount of money. However, the downside is that you’ll face higher interest rates and larger monthly payments once the loan officially begins. This type of mortgages is suitable for people who have a steady income and plan to stay in their home for a long time.

7. JOINT MORTGAGE

A joint mortgage allows two or more people to borrow and repay the loan together. This is a popular option for couples or those with financial support from relatives.

The advantage of a joint mortgage is that two people can combine their incomes to increase their borrowing capacity and reduce financial pressure. However, the disadvantage is that if one of the two people experiences financial difficulties, this can affect both of their ability to repay the loan.